How to Self-Manage Rental Property: The Complete Guide for 1 to 100 Units

How to Self-Manage Rental Property: The Complete Guide for 1 to 100 Units

How to self-manage rental property is the operational question behind every landlord's decision to skip hiring a property manager. Self-managing means you directly handle tenant screening, lease creation, rent collection, maintenance coordination, communication, bookkeeping, and compliance across your portfolio. For landlords with 1 to 100 units, self-management can save thousands annually in PM fees, but only if you run it as a repeatable system rather than a reactive side task.

This guide is part of the self-managing vs. hiring a property manager decision series for independent landlords.

This guide maps every core responsibility, gives you standardized workflows for each one, and shows how the process scales as your portfolio grows. It connects to the full self-managing vs. hiring a property manager decision framework and pairs with the true cost breakdown of hiring a PM so you can compare both paths with real numbers.

What Self-Management Actually Includes

Self-managing means you handle the core functions a property manager normally performs: marketing and inquiries, tenant screening and selection, lease creation and enforcement, rent collection and delinquency workflow, maintenance triage and vendor coordination, tenant communication and documentation, bookkeeping and tax-ready records, and legal compliance and renewals.

Workload reality. The first 1 to 3 units often feel manageable because events are occasional. The challenge starts when tasks overlap: two renewals, one late payer, one emergency repair, and a vacancy all at once. The solution is not working harder. It is standardizing your process.

Cost reality. Most professional management models charge 8% to 12% of collected rent plus leasing, renewal fees, and other add-ons. DIY can save that fee load, but only if you avoid hidden costs like poor screening (leading to evictions), slow maintenance response (bigger repairs and unhappy tenants), and disorganized records (tax headaches). See the true cost breakdown for full dollar math.

For the full all-in annual cost breakdown of professional management, see the true cost of hiring a property manager.

Risk reality. Evictions are the big financial landmine. Research summaries cite eviction totals ranging from $3,500 to $10,000 or more once you add legal fees, lost rent, and turnover costs. That is why screening and documentation are not "admin" tasks. They are your primary risk controls.

The modern advantage. Digital payments, online maintenance requests, templated messaging, and centralized document storage reduce time and increase consistency. A solid all-in-one platform becomes your virtual property management office: workflows, reminders, audit trails, and clean books. For a breakdown of what to look for in that platform, see Best Property Management Software for Small Landlords.

Self-managing successfully requires the right tools. See our comparison of property management software for small landlords to find a platform that handles the heavy lifting.

Tenant Screening: Your Number One Risk Control

Tenant screening is where profitability is won or lost. A single poor placement can lead to chronic late payments, property damage, or eviction, with costs commonly cited at $3,500 to $10,000 or more. Screening is also where landlords most commonly feel uncertain. Industry surveys consistently show screening as one of the top challenges landlords report.

For a breakdown of which tasks require professional support, see what property managers actually do.

Workflow You Can Standardize

Publish written criteria first. Define income multiple, credit expectations, rental history standards, occupancy limits, and any deal-breakers. Apply criteria consistently to every applicant.

Pre-screen with the same questions for everyone. Example questions: move-in date, number of occupants, pets, smoking, and whether they can verify income.

Run credit, background, and eviction checks. Use reputable screening reports and read them in context, not just the score. Verify income and employment through pay stubs, bank statements, or offer letters. Confirm employer contact when appropriate.

Verify rental history. Call prior landlords and cross-check dates and payment behavior. Document the decision. Keep your notes and adverse action steps if you deny based on report data.

Fair Housing and Screening Compliance

Federal Fair Housing law prohibits discrimination based on race, color, religion, sex, disability, familial status, and national origin. HUD has also warned that overly broad screening practices, including blanket criminal history policies, can create discriminatory effects. Many states add additional protected classes, including source-of-income protections in some jurisdictions. Use consistent criteria and be prepared to explain how each criterion relates to legitimate risk.

Practical Applications

An applicant with a moderate credit score due to medical debt but perfect rent history may be a stronger candidate than someone with a higher score but multiple landlord complaints. A consistent, holistic process can outperform score-only decisions.

As you scale from a few units to a dozen or more, standardizing criteria and using digital applications ensures every file is complete and time-stamped, reducing gut-feel decisions that create liability.

Actionable step: Build a one-page screening rubric covering income, rent history, collections, eviction record, and references. Require yourself to fill it out before approving anyone.

How software helps. Online applications, automated identity checks, and stored screening criteria reduce bias, speed approvals, and keep an audit trail.

Lease Creation and Ongoing Lease Management

Your lease is the operating manual for the landlord-tenant relationship. Most disputes come down to unclear expectations: when rent is due, who pays utilities, how maintenance is requested, what happens with unauthorized occupants, and how notices are delivered.

Lease Essentials to Lock Down

Cover these in every lease: parties, term, rent amount, and due date. Late fees and returned payment policy within state limits. Security deposit terms and move-out process. Maintenance responsibilities and reporting method. Entry notice policy and emergency access rules, which are state-specific.

Also include rules on smoking, pets, parking, noise, and subletting. Add fee disclosures and addenda such as lead-based paint disclosure for pre-1978 properties.

Management Workflow

Use a standard lease template per property type (single-family vs. multi). Add property-specific addenda: utilities, HOA rules, pet policy, parking map. Execute via e-signature and store the signed PDF with all addenda in one place. Set reminders for lease end date, renewal window, rent increase notice window, and inspection schedule.

Practical Applications

A duplex landlord includes a utilities addendum specifying who pays water and sewer and how usage is allocated. The potential dispute never starts because expectations were explicit from day one.

An 18-unit owner uses one master lease plus unit addenda, reducing mistakes during turnover and keeping language consistent across the portfolio.

Actionable step: Maintain a lease change log. If you update your lease language due to a lesson learned (parking, trash, quiet hours), log the change so future leases stay consistent.

How software helps. Template leases, e-sign, and centralized document storage reduce omissions and make renewals fast.

Rent Collection and Delinquency Management

Late rent is rarely solved by more reminders alone. It is solved by removing friction and having a predictable policy. Industry consumer research consistently shows strong preference for digital payment interactions among both landlords and renters.

Best-Practice Rent Collection System

Offer at least one digital payment option such as bank transfer or ACH. Automate reminders: pre-due, due-day, and grace-period-ending. Enforce a consistent late-fee policy within legal limits. Escalate with documented notices if unpaid.

Moving from checks and cash to ACH autopay is one of the highest-impact changes a self-managing landlord can make. Tenants stop relying on memory and mail timing. Track your late-payment rate before and after adoption and adjust your reminder cadence based on the data.

A landlord managing 6 units who stops accepting cash and documents a single payment policy reduces disputes about whether payments were made. At 25 units, auto-late fees and auto-ledger posting turn delinquencies into a weekly report instead of daily stress.

Actionable step: Track a simple KPI: percent paid by the 3rd. If it drops, review which tenants are not on digital payments and proactively offer setup help.

How software helps. Automated invoicing, recurring payments, ledger posting, and delinquency workflows reduce time and create a clean record if you ever need to enforce the lease.

Rent Reminder Cadence Template

Day minus 3: friendly reminder plus payment link. Day 1: rent due confirmation. Day 3 (end of grace period, if applicable): late notice plus late fee disclosure within legal limits. Day 5 to 7: formal pay-or-quit notice if unpaid (jurisdiction-specific).

Maintenance Coordination

Maintenance is where landlords feel the most pressure. Industry data consistently ranks maintenance and ongoing management among the most prominent operational challenges. It is also where reputations are made: prompt, documented responses build retention.

Triage Workflow

Categorize every request. Emergency: water leak, no heat in winter, electrical hazard. Urgent: appliance failure, clogged main line. Routine: dripping faucet, cosmetic issue.

Respond with a timeline. "We have received your request. Next update by [specific time]." Dispatch vendor using a preferred vendor list with after-hours options. Document everything: photos, invoices, and tenant communications. Close out by confirming resolution with the tenant and noting any preventive follow-up.

Practical Applications

A tenant reports a "small drip." The landlord requests a photo through the maintenance portal and classifies it as urgent. A $180 repair prevents a ceiling collapse that would have cost significantly more.

Building an emergency instruction sheet with shutoff valve locations and a vendor hotline turns middle-of-the-night calls into structured events instead of panic.

Actionable step: Build a not-to-exceed repair authorization limit (for example, $300) for trusted vendors so emergencies do not stall waiting for your approval.

How software helps. Centralized work orders, vendor assignment, status tracking, and stored invoices support faster response and better budgeting.

Maintenance Triage Quick Guide

Emergency (active leak, no heat in cold weather, electrical hazard): respond immediately, dispatch vendor. Urgent (fridge down, clogged main line): respond same day, schedule within 24 to 48 hours. Routine (minor drip, cosmetic issue): respond within 24 hours, schedule within 7 to 14 days.

Tenant Communication

Tenant communication is not about being available around the clock. It is about being reliable, consistent, and documented. Digital-first workflows align with renter preferences for online communication and reduce misunderstandings.

Communication System You Can Run

Designate one official channel for non-emergencies (portal or email). Post clear hours and emergency rules in the lease welcome packet. Build templates for common messages: rent reminders, inspection notices, maintenance updates. Keep a log of all material conversations including repairs, complaints, and warnings.

Practical Applications

A noise complaint comes in. The landlord replies with a template: acknowledges the issue, requests dates and times, reminds both parties of quiet hours, and documents the warning if needed. The process is the same every time, regardless of which tenant or property is involved.

After a plumber visit, sending a two-question check-in ("Resolved? Any remaining issue?") closes the loop and reduces repeat tickets.

Actionable step: Use a 24-4-24 cadence: acknowledge within 24 hours, provide a plan within 4 business hours for urgent items, and confirm closure within 24 hours of completion.

How software helps. Message templates, conversation-to-unit linking, and searchable communication history keep interactions professional and documented.

Bookkeeping and Tax Prep

Bookkeeping is where DIY landlords quietly lose time, then scramble at tax season. If you self-manage, the goal is simple: every dollar should be categorized, traceable, and tied to a property or unit.

Core Accounting Workflow

Separate finances with a dedicated bank account per entity or portfolio. Categorize transactions monthly: rent, fees, repairs, capital expenditures, utilities, insurance, and taxes. Attach source documents: invoices, receipts, and lease ledgers. Reconcile monthly by comparing bank statements against your ledger. Run reports quarterly: income statement by property, delinquency, and maintenance spend.

Practical Applications

A landlord sees rising maintenance costs but cannot pinpoint why. After categorizing by vendor and system (plumbing vs. HVAC), they spot repeat drain clogs and schedule preventive jetting, turning a reactive cost into a planned one.

Tracking vacancy paint and cleaning costs separately reveals that one unit's turnover is consistently higher than others, leading to a durable flooring upgrade decision that reduces future turnover expense.

Actionable step: Close your books on the 5th of each month. Put a recurring calendar block: "Reconcile and attach receipts."

How software helps. Automated rent ledger entries, receipt capture, property-level reporting, and exportable year-end summaries reduce tax-time stress.

Legal Compliance and Fair Housing

Legal compliance is the part most owners fear because it is high stakes and highly local. You do not need to memorize everything. You need a system that forces consistency and documentation.

Fair Housing Essentials

Federal Fair Housing protections include race, color, religion, sex, disability, familial status, and national origin. HUD guidance highlights risks when screening tools, including algorithmic approaches, create discriminatory effects and stresses careful policy design and oversight. Many states and cities add protected classes, including source-of-income protections in some areas. This is why standardized criteria and consistent application matter.

Operational Compliance Areas to Systematize

Proper notices (entry, late rent, non-renewal) in the required format and timing. Security deposit handling and itemization rules, which are state-specific. Habitability obligations and timely repairs. Advertising language consistency to avoid exclusionary phrasing.

Practical Applications

Two applicants apply. The landlord uses the same written rubric and keeps decision notes. When the denied applicant asks why, the landlord can point to objective criteria applied consistently.

A landlord in a jurisdiction with source-of-income protections updates advertising and screening to avoid blanket refusal language.

Actionable step: Create a compliance folder per property: statutes and links, notice templates, deposit rules summary, and a timeline checklist. Review annually.

How software helps. Standardized application flow, stored documentation, and templated notices reduce missed steps and support defensible decisions.

Lease Renewals, Rent Increases, and Retention

Renewals are where self-managers can outperform professional PMs: quicker decisions, better tenant relationships, and fewer unnecessary vacancies. Retention is also one of the most effective ways to reduce overall property management costs since every avoided turnover eliminates placement fees, vacancy loss, and make-ready expenses.

Renewal Workflow

Start 90 to 120 days before lease end. Evaluate tenant performance: on-time payments, care of unit, communication responsiveness. Run a quick market check on comparable rents and cost pressures like insurance, taxes, and repairs.

Send a renewal offer with options. Offering both a 12-month term with a moderate increase and a 24-month term with a smaller increase gives tenants a sense of control and reduces the chance of non-renewal.

If non-renewing, start make-ready planning immediately: vendors, showing windows, and listing photos.

Actionable step: Create a renewal scorecard covering payment history, maintenance burden, neighbor complaints, and inspection results. Use it to decide "renew, renew with conditions, or non-renew" consistently.

How software helps. Automated lease-end reminders, renewal templates, e-sign, and rent-roll reporting make renewals manageable even as unit count grows. For platforms that include early renewal polling, landlords get visibility into tenant intentions months before the lease ends rather than days. See Essential Systems for Self-Managing Landlords for a full breakdown of operational tools.

If you are transitioning away from a PM, see how to switch from a property manager to self-managing for the full handoff guide.

Monthly Operating Checklist

Use this as your baseline operating checklist for how to self-manage rental property tasks without dropping the ball.

Reconcile rent ledger against bank deposits. Review delinquencies and send reminders per policy. Review open maintenance tickets and close with confirmation. Spot-check communications for documentation completeness. Update KPI dashboard: percent paid by 3rd, response time, and vacancy rate.

Frequently Asked Questions

Is it realistic to self-manage more than 10 units?

Yes, if you standardize workflows and centralize communication, payments, documents, and maintenance into one system. The ceiling for self-management has risen significantly with digital tools. Most landlords who struggle past 10 units are fighting process problems, not volume problems.

How much do I actually save by not hiring a property manager?

Typical management fees of 8% to 12% of collected rent plus leasing fees, setup fees, and maintenance markups can total 15% to 25% of scheduled rent annually. DIY savings are meaningful only if your systems prevent costly errors like poor screening or delayed maintenance.

What is the biggest legal risk when self-managing?

Inconsistent screening and communication are the primary risk multipliers. Federal Fair Housing protections apply nationwide, and HUD has cautioned about screening practices that can create discriminatory effects. Use written criteria, apply them consistently, and document every decision.

What is the single best way to reduce eviction risk?

Rigorous, consistent screening and documentation. Evictions can cost $3,500 to $10,000 or more in combined expenses, so preventing even one problem tenancy can pay for years of better processes.

When does self-managing stop making sense?

Self-managing stops making sense when you consistently miss response-time goals, when renewals and rent increases slip because you are too busy, or when your portfolio grows beyond your operational capacity. See When to Hire a Property Manager for a structured decision framework.

How to Self-Manage Rental Property: The Complete Guide for 1 to 100 Units

How to self-manage rental property is the operational question behind every landlord's decision to skip hiring a property manager. Self-managing means you directly handle tenant screening, lease creation, rent collection, maintenance coordination, communication, bookkeeping, and compliance across your portfolio. For landlords with 1 to 100 units, self-management can save thousands annually in PM fees, but only if you run it as a repeatable system rather than a reactive side task.

This guide is part of the self-managing vs. hiring a property manager decision series for independent landlords.

This guide maps every core responsibility, gives you standardized workflows for each one, and shows how the process scales as your portfolio grows. It connects to the full self-managing vs. hiring a property manager decision framework and pairs with the true cost breakdown of hiring a PM so you can compare both paths with real numbers.

What Self-Management Actually Includes

Self-managing means you handle the core functions a property manager normally performs: marketing and inquiries, tenant screening and selection, lease creation and enforcement, rent collection and delinquency workflow, maintenance triage and vendor coordination, tenant communication and documentation, bookkeeping and tax-ready records, and legal compliance and renewals.

Workload reality. The first 1 to 3 units often feel manageable because events are occasional. The challenge starts when tasks overlap: two renewals, one late payer, one emergency repair, and a vacancy all at once. The solution is not working harder. It is standardizing your process.

Cost reality. Most professional management models charge 8% to 12% of collected rent plus leasing, renewal fees, and other add-ons. DIY can save that fee load, but only if you avoid hidden costs like poor screening (leading to evictions), slow maintenance response (bigger repairs and unhappy tenants), and disorganized records (tax headaches). See the true cost breakdown for full dollar math.

For the full all-in annual cost breakdown of professional management, see the true cost of hiring a property manager.

Risk reality. Evictions are the big financial landmine. Research summaries cite eviction totals ranging from $3,500 to $10,000 or more once you add legal fees, lost rent, and turnover costs. That is why screening and documentation are not "admin" tasks. They are your primary risk controls.

The modern advantage. Digital payments, online maintenance requests, templated messaging, and centralized document storage reduce time and increase consistency. A solid all-in-one platform becomes your virtual property management office: workflows, reminders, audit trails, and clean books. For a breakdown of what to look for in that platform, see Best Property Management Software for Small Landlords.

Self-managing successfully requires the right tools. See our comparison of property management software for small landlords to find a platform that handles the heavy lifting.

Tenant Screening: Your Number One Risk Control

Tenant screening is where profitability is won or lost. A single poor placement can lead to chronic late payments, property damage, or eviction, with costs commonly cited at $3,500 to $10,000 or more. Screening is also where landlords most commonly feel uncertain. Industry surveys consistently show screening as one of the top challenges landlords report.

For a breakdown of which tasks require professional support, see what property managers actually do.

Workflow You Can Standardize

Publish written criteria first. Define income multiple, credit expectations, rental history standards, occupancy limits, and any deal-breakers. Apply criteria consistently to every applicant.

Pre-screen with the same questions for everyone. Example questions: move-in date, number of occupants, pets, smoking, and whether they can verify income.

Run credit, background, and eviction checks. Use reputable screening reports and read them in context, not just the score. Verify income and employment through pay stubs, bank statements, or offer letters. Confirm employer contact when appropriate.

Verify rental history. Call prior landlords and cross-check dates and payment behavior. Document the decision. Keep your notes and adverse action steps if you deny based on report data.

Fair Housing and Screening Compliance

Federal Fair Housing law prohibits discrimination based on race, color, religion, sex, disability, familial status, and national origin. HUD has also warned that overly broad screening practices, including blanket criminal history policies, can create discriminatory effects. Many states add additional protected classes, including source-of-income protections in some jurisdictions. Use consistent criteria and be prepared to explain how each criterion relates to legitimate risk.

Practical Applications

An applicant with a moderate credit score due to medical debt but perfect rent history may be a stronger candidate than someone with a higher score but multiple landlord complaints. A consistent, holistic process can outperform score-only decisions.

As you scale from a few units to a dozen or more, standardizing criteria and using digital applications ensures every file is complete and time-stamped, reducing gut-feel decisions that create liability.

Actionable step: Build a one-page screening rubric covering income, rent history, collections, eviction record, and references. Require yourself to fill it out before approving anyone.

How software helps. Online applications, automated identity checks, and stored screening criteria reduce bias, speed approvals, and keep an audit trail.

Lease Creation and Ongoing Lease Management

Your lease is the operating manual for the landlord-tenant relationship. Most disputes come down to unclear expectations: when rent is due, who pays utilities, how maintenance is requested, what happens with unauthorized occupants, and how notices are delivered.

Lease Essentials to Lock Down

Cover these in every lease: parties, term, rent amount, and due date. Late fees and returned payment policy within state limits. Security deposit terms and move-out process. Maintenance responsibilities and reporting method. Entry notice policy and emergency access rules, which are state-specific.

Also include rules on smoking, pets, parking, noise, and subletting. Add fee disclosures and addenda such as lead-based paint disclosure for pre-1978 properties.

Management Workflow

Use a standard lease template per property type (single-family vs. multi). Add property-specific addenda: utilities, HOA rules, pet policy, parking map. Execute via e-signature and store the signed PDF with all addenda in one place. Set reminders for lease end date, renewal window, rent increase notice window, and inspection schedule.

Practical Applications

A duplex landlord includes a utilities addendum specifying who pays water and sewer and how usage is allocated. The potential dispute never starts because expectations were explicit from day one.

An 18-unit owner uses one master lease plus unit addenda, reducing mistakes during turnover and keeping language consistent across the portfolio.

Actionable step: Maintain a lease change log. If you update your lease language due to a lesson learned (parking, trash, quiet hours), log the change so future leases stay consistent.

How software helps. Template leases, e-sign, and centralized document storage reduce omissions and make renewals fast.

Rent Collection and Delinquency Management

Late rent is rarely solved by more reminders alone. It is solved by removing friction and having a predictable policy. Industry consumer research consistently shows strong preference for digital payment interactions among both landlords and renters.

Best-Practice Rent Collection System

Offer at least one digital payment option such as bank transfer or ACH. Automate reminders: pre-due, due-day, and grace-period-ending. Enforce a consistent late-fee policy within legal limits. Escalate with documented notices if unpaid.

Moving from checks and cash to ACH autopay is one of the highest-impact changes a self-managing landlord can make. Tenants stop relying on memory and mail timing. Track your late-payment rate before and after adoption and adjust your reminder cadence based on the data.

A landlord managing 6 units who stops accepting cash and documents a single payment policy reduces disputes about whether payments were made. At 25 units, auto-late fees and auto-ledger posting turn delinquencies into a weekly report instead of daily stress.

Actionable step: Track a simple KPI: percent paid by the 3rd. If it drops, review which tenants are not on digital payments and proactively offer setup help.

How software helps. Automated invoicing, recurring payments, ledger posting, and delinquency workflows reduce time and create a clean record if you ever need to enforce the lease.

Rent Reminder Cadence Template

Day minus 3: friendly reminder plus payment link. Day 1: rent due confirmation. Day 3 (end of grace period, if applicable): late notice plus late fee disclosure within legal limits. Day 5 to 7: formal pay-or-quit notice if unpaid (jurisdiction-specific).

Maintenance Coordination

Maintenance is where landlords feel the most pressure. Industry data consistently ranks maintenance and ongoing management among the most prominent operational challenges. It is also where reputations are made: prompt, documented responses build retention.

Triage Workflow

Categorize every request. Emergency: water leak, no heat in winter, electrical hazard. Urgent: appliance failure, clogged main line. Routine: dripping faucet, cosmetic issue.

Respond with a timeline. "We have received your request. Next update by [specific time]." Dispatch vendor using a preferred vendor list with after-hours options. Document everything: photos, invoices, and tenant communications. Close out by confirming resolution with the tenant and noting any preventive follow-up.

Practical Applications

A tenant reports a "small drip." The landlord requests a photo through the maintenance portal and classifies it as urgent. A $180 repair prevents a ceiling collapse that would have cost significantly more.

Building an emergency instruction sheet with shutoff valve locations and a vendor hotline turns middle-of-the-night calls into structured events instead of panic.

Actionable step: Build a not-to-exceed repair authorization limit (for example, $300) for trusted vendors so emergencies do not stall waiting for your approval.

How software helps. Centralized work orders, vendor assignment, status tracking, and stored invoices support faster response and better budgeting.

Maintenance Triage Quick Guide

Emergency (active leak, no heat in cold weather, electrical hazard): respond immediately, dispatch vendor. Urgent (fridge down, clogged main line): respond same day, schedule within 24 to 48 hours. Routine (minor drip, cosmetic issue): respond within 24 hours, schedule within 7 to 14 days.

Tenant Communication

Tenant communication is not about being available around the clock. It is about being reliable, consistent, and documented. Digital-first workflows align with renter preferences for online communication and reduce misunderstandings.

Communication System You Can Run

Designate one official channel for non-emergencies (portal or email). Post clear hours and emergency rules in the lease welcome packet. Build templates for common messages: rent reminders, inspection notices, maintenance updates. Keep a log of all material conversations including repairs, complaints, and warnings.

Practical Applications

A noise complaint comes in. The landlord replies with a template: acknowledges the issue, requests dates and times, reminds both parties of quiet hours, and documents the warning if needed. The process is the same every time, regardless of which tenant or property is involved.

After a plumber visit, sending a two-question check-in ("Resolved? Any remaining issue?") closes the loop and reduces repeat tickets.

Actionable step: Use a 24-4-24 cadence: acknowledge within 24 hours, provide a plan within 4 business hours for urgent items, and confirm closure within 24 hours of completion.

How software helps. Message templates, conversation-to-unit linking, and searchable communication history keep interactions professional and documented.

Bookkeeping and Tax Prep

Bookkeeping is where DIY landlords quietly lose time, then scramble at tax season. If you self-manage, the goal is simple: every dollar should be categorized, traceable, and tied to a property or unit.

Core Accounting Workflow

Separate finances with a dedicated bank account per entity or portfolio. Categorize transactions monthly: rent, fees, repairs, capital expenditures, utilities, insurance, and taxes. Attach source documents: invoices, receipts, and lease ledgers. Reconcile monthly by comparing bank statements against your ledger. Run reports quarterly: income statement by property, delinquency, and maintenance spend.

Practical Applications

A landlord sees rising maintenance costs but cannot pinpoint why. After categorizing by vendor and system (plumbing vs. HVAC), they spot repeat drain clogs and schedule preventive jetting, turning a reactive cost into a planned one.

Tracking vacancy paint and cleaning costs separately reveals that one unit's turnover is consistently higher than others, leading to a durable flooring upgrade decision that reduces future turnover expense.

Actionable step: Close your books on the 5th of each month. Put a recurring calendar block: "Reconcile and attach receipts."

How software helps. Automated rent ledger entries, receipt capture, property-level reporting, and exportable year-end summaries reduce tax-time stress.

Legal Compliance and Fair Housing

Legal compliance is the part most owners fear because it is high stakes and highly local. You do not need to memorize everything. You need a system that forces consistency and documentation.

Fair Housing Essentials

Federal Fair Housing protections include race, color, religion, sex, disability, familial status, and national origin. HUD guidance highlights risks when screening tools, including algorithmic approaches, create discriminatory effects and stresses careful policy design and oversight. Many states and cities add protected classes, including source-of-income protections in some areas. This is why standardized criteria and consistent application matter.

Operational Compliance Areas to Systematize

Proper notices (entry, late rent, non-renewal) in the required format and timing. Security deposit handling and itemization rules, which are state-specific. Habitability obligations and timely repairs. Advertising language consistency to avoid exclusionary phrasing.

Practical Applications

Two applicants apply. The landlord uses the same written rubric and keeps decision notes. When the denied applicant asks why, the landlord can point to objective criteria applied consistently.

A landlord in a jurisdiction with source-of-income protections updates advertising and screening to avoid blanket refusal language.

Actionable step: Create a compliance folder per property: statutes and links, notice templates, deposit rules summary, and a timeline checklist. Review annually.

How software helps. Standardized application flow, stored documentation, and templated notices reduce missed steps and support defensible decisions.

Lease Renewals, Rent Increases, and Retention

Renewals are where self-managers can outperform professional PMs: quicker decisions, better tenant relationships, and fewer unnecessary vacancies. Retention is also one of the most effective ways to reduce overall property management costs since every avoided turnover eliminates placement fees, vacancy loss, and make-ready expenses.

Renewal Workflow

Start 90 to 120 days before lease end. Evaluate tenant performance: on-time payments, care of unit, communication responsiveness. Run a quick market check on comparable rents and cost pressures like insurance, taxes, and repairs.

Send a renewal offer with options. Offering both a 12-month term with a moderate increase and a 24-month term with a smaller increase gives tenants a sense of control and reduces the chance of non-renewal.

If non-renewing, start make-ready planning immediately: vendors, showing windows, and listing photos.

Actionable step: Create a renewal scorecard covering payment history, maintenance burden, neighbor complaints, and inspection results. Use it to decide "renew, renew with conditions, or non-renew" consistently.

How software helps. Automated lease-end reminders, renewal templates, e-sign, and rent-roll reporting make renewals manageable even as unit count grows. For platforms that include early renewal polling, landlords get visibility into tenant intentions months before the lease ends rather than days. See Essential Systems for Self-Managing Landlords for a full breakdown of operational tools.

If you are transitioning away from a PM, see how to switch from a property manager to self-managing for the full handoff guide.

Monthly Operating Checklist

Use this as your baseline operating checklist for how to self-manage rental property tasks without dropping the ball.

Reconcile rent ledger against bank deposits. Review delinquencies and send reminders per policy. Review open maintenance tickets and close with confirmation. Spot-check communications for documentation completeness. Update KPI dashboard: percent paid by 3rd, response time, and vacancy rate.

Frequently Asked Questions

Is it realistic to self-manage more than 10 units?

Yes, if you standardize workflows and centralize communication, payments, documents, and maintenance into one system. The ceiling for self-management has risen significantly with digital tools. Most landlords who struggle past 10 units are fighting process problems, not volume problems.

How much do I actually save by not hiring a property manager?

Typical management fees of 8% to 12% of collected rent plus leasing fees, setup fees, and maintenance markups can total 15% to 25% of scheduled rent annually. DIY savings are meaningful only if your systems prevent costly errors like poor screening or delayed maintenance.

What is the biggest legal risk when self-managing?

Inconsistent screening and communication are the primary risk multipliers. Federal Fair Housing protections apply nationwide, and HUD has cautioned about screening practices that can create discriminatory effects. Use written criteria, apply them consistently, and document every decision.

What is the single best way to reduce eviction risk?

Rigorous, consistent screening and documentation. Evictions can cost $3,500 to $10,000 or more in combined expenses, so preventing even one problem tenancy can pay for years of better processes.

When does self-managing stop making sense?

Self-managing stops making sense when you consistently miss response-time goals, when renewals and rent increases slip because you are too busy, or when your portfolio grows beyond your operational capacity. See When to Hire a Property Manager for a structured decision framework.

{

"@context": "https://schema.org",

"@type": "FAQPage",

"mainEntity": [

{

"@type": "Question",

"name": "Is it realistic to self-manage more than 10 units?",

"acceptedAnswer": {

"@type": "Answer",

"text": "Yes, if you standardize workflows and centralize communication, payments, documents, and maintenance into one system. The ceiling for self-management has risen significantly with digital tools. Most landlords who struggle past 10 units are fighting process problems, not volume problems."

}

},

{

"@type": "Question",

"name": "How much do I actually save by not hiring a property manager?",

"acceptedAnswer": {

"@type": "Answer",

"text": "Typical management fees of 8% to 12% of collected rent plus leasing fees, setup fees, and maintenance markups can total 15% to 25% of scheduled rent annually. DIY savings are meaningful only if your systems prevent costly errors like poor screening or delayed maintenance."

}

},

{

"@type": "Question",

"name": "What is the biggest legal risk when self-managing?",

"acceptedAnswer": {

"@type": "Answer",

"text": "Inconsistent screening and communication are the primary risk multipliers. Federal Fair Housing protections apply nationwide, and HUD has cautioned about screening practices that can create discriminatory effects. Use written criteria, apply them consistently, and document every decision."

}

},

{

"@type": "Question",

"name": "What is the single best way to reduce eviction risk?",

"acceptedAnswer": {

"@type": "Answer",

"text": "Rigorous, consistent screening and documentation. Evictions can cost $3,500 to $10,000 or more in combined expenses, so preventing even one problem tenancy can pay for years of better processes."

}

},

{

"@type": "Question",

"name": "When does self-managing stop making sense?",

"acceptedAnswer": {

"@type": "Answer",

"text": "Self-managing stops making sense when you consistently miss response-time goals, when renewals and rent increases slip because you are too busy, or when your portfolio grows beyond your operational capacity."

}

}

]

}

Shuk helps landlords and property managers get ahead of vacancies, improve renewal visibility, and bring more predictability to every lease cycle.

Book a demo to get started with a free trial.

Common Screening Mistakes: Tenant Screening Errors Landlords Make and How to Fix Them

Tenant screening is the process of evaluating rental applicants through credit checks, background reports, income verification, eviction history, and reference validation before approving a lease. It helps independent landlords and small property managers reduce default risk, avoid costly evictions, and maintain consistent occupancy. For landlords managing 1–100 units, a standardized screening workflow is one of the most effective ways to protect rental income.

Why Screening Mistakes Are Costly for Small Landlords

Screening errors create direct financial exposure. A typical eviction costs several thousand dollars in direct expenses, with complex cases reaching significantly more. Turnover and make-ready costs add further losses per unit. For small-portfolio landlords, a single bad placement can eliminate months of profit.

The risk environment is also shifting. Eviction filings have increased nationally in recent years, and application fraud continues to grow as a concern for property operators.

Most of these outcomes trace back to preventable process gaps: skipping eviction history, applying inconsistent standards, missing fraud signals, or mishandling Fair Housing and FCRA requirements.

10 Tenant Screening Mistakes Landlords Make

1. Screening Without Written, Consistent Criteria

Deciding "case by case" without a documented tenant selection policy creates Fair Housing exposure and operational inconsistency. The Fair Housing Act prohibits discrimination on protected-class grounds, and uneven application of criteria is a common fact pattern in complaints.

A landlord who requires a 650 credit score for one applicant but accepts 580 for another has no defensible standard if a denied applicant alleges discriminatory treatment. In some states, landlords must disclose tenant selection criteria by law, making informal screening a direct compliance issue.

How to fix it:

- Create written criteria covering income multiples, credit thresholds, rental history requirements, eviction history rules, criminal history approach (aligned to local law), and occupancy limits.

- Train anyone involved in leasing to follow the same rubric.

- Document all exceptions with objective compensating factors (e.g., additional qualified co-signer where legal).

If you cannot explain your approval or denial in two sentences using written criteria, you are exposed.

2. Skipping Eviction History Screening

Running credit and criminal checks without consistently checking eviction filings and judgments leaves a major gap. Evictions are a leading indicator of nonpayment and lease conflict, and national eviction data remains limited, which means landlords who skip this step are operating without critical information.

A tenant with a decent credit score may still have two prior eviction filings that were settled or dismissed. Without eviction history screening tied to identity verification, those patterns go undetected. A tenant using a slightly different name spelling can bypass checks entirely if identity matching is weak.

How to fix it:

- Make eviction history screening mandatory for every adult applicant.

- Review filings, not just judgments. Patterns of filings reveal risk even when cases do not result in a formal judgment.

- Pair eviction checks with identity verification so records match the correct person.

3. Over-Relying on Credit Score

Using a hard credit-score cutoff without analyzing the broader risk profile misses important context. Credit scores were built for credit risk, not rental performance. Rental payment history is a stronger predictor of tenant reliability than a general credit score alone.

An applicant with a 700 score but recent late payments and high revolving utilization may be a higher risk than an applicant with a 630 score, stable rent payment history, and low debt. A medical collection dragging down an otherwise stable applicant can cause a rigid cutoff to reject a likely reliable tenant and extend vacancy. A thin-file applicant with strong verified income and references gets denied under a score-only rule despite low actual risk.

How to fix it:

- Evaluate income stability, verified rent-to-income ratio, rental history, eviction history, and credit tradeline quality alongside the score.

- Define which derogatories are disqualifying (e.g., landlord-related collections) and which require context (e.g., old medical debt), consistent with local rules and Fair Housing risk analysis.

The question is not "What is the score?" It is "What does this report predict about paying rent and honoring the lease?"

4. Inadequate Income Verification

Accepting screenshots, editable PDFs, or unverifiable employer letters without third-party verification is a growing liability. Application fraud is an increasing concern across the rental industry, and fraudulent income documentation is one of the most common vectors. Fraud leads directly to nonpayment, eviction filings, and bad debt.

Common fraud patterns include pay stubs with mismatched YTD totals, "employer" phone numbers that route to a friend, bank statements showing recent large transfers rather than recurring income, and offer letters with start dates that never materialize.

How to fix it:

- Require a standard income package by income type (W-2, 1099, self-employed, fixed income).

- Verify employment through independent channels (company main line found independently, not applicant-provided).

- Cross-check pay frequency, YTD math, bank deposit patterns, and stated position and salary.

If a document can be edited, assume it will be edited until verified.

5. DIY Background Checks That Violate the FCRA

Running online searches or purchasing non-compliant reports without proper disclosures, authorization, permissible purpose, and adverse action steps creates legal exposure. The FCRA requires a permissible purpose and specific disclosure and authorization steps when obtaining consumer reports for housing decisions. Regulators have emphasized both the permissible purpose requirement and the duty to provide adverse action notices when denying based on a report.

Screening data can also be wrong. Enforcement actions against tenant screening companies tied to FCRA compliance and accuracy issues have resulted in significant settlements. A report that mixes records from two people with similar names creates liability if the landlord acts on incorrect data without allowing dispute time.

How to fix it:

- Use FCRA-aligned workflows: written disclosure, written authorization, documented permissible purpose, and compliant adverse action notices.

- Verify identifiers (date of birth, SSN match logic where available, address history) before acting on negative items.

- Build a dispute and clarification step into your process.

Compliance is not paperwork. It is your shield when an applicant challenges your decision.

6. Mishandling Criminal History

Denying any applicant with any criminal record or applying blanket "crime-free" rules without nuance creates significant legal risk. HUD has warned that blanket criminal record bans can create discriminatory effects (disparate impact) under the Fair Housing Act. Local laws can further restrict what landlords may consider. Several jurisdictions now require individualized assessment before adverse decisions based on criminal history.

Denying based on an arrest record rather than a conviction is particularly problematic. Arrest-only information is often unreliable as a predictor and can amplify fairness and accuracy concerns.

How to fix it:

- Check state and city rules first, especially in "fair chance" jurisdictions.

- Use individualized assessment factors: nature and severity of the offense, time elapsed, evidence of rehabilitation, and relevance to housing safety.

- Document the analysis and apply it consistently.

7. Ignoring Source-of-Income Protections

Rejecting applicants because they use housing assistance, vouchers, or nontraditional lawful income is illegal in many jurisdictions. Multiple states and cities explicitly treat voucher income as a protected source of income. Screening policies that disadvantage voucher holders have triggered litigation and settlements.

Common violations include stating "we don't accept vouchers" in a protected jurisdiction, requiring voucher holders to meet higher credit thresholds than non-voucher applicants, and excluding the subsidy portion when calculating income.

How to fix it:

- Treat lawful assistance as income when required by local law and apply the same screening standards to all applicants.

- Use consistent rent-to-income calculations that reflect the tenant portion vs. total rent where appropriate.

- Train staff on local source-of-income rules.

If your criteria change based on where the money comes from rather than whether it is reliable and lawful, you are inviting legal risk.

8. Failing to Document Decisions

Screening without saving reports, decision notes, reasons for denial, or proof of consistent criteria application leaves you defenseless in a dispute. The FCRA requires specific steps when taking adverse action based on a consumer report, and documentation proves you followed them.

If two applicants are denied for "credit" but you cannot show which tradelines or thresholds drove each decision, your consistency is unverifiable. If an applicant disputes inaccurate information and you have no saved copy of the report or adverse action notice, you cannot demonstrate compliance.

How to fix it:

- Maintain a standardized screening file for each applicant: application, ID verification steps, income documents, rental references, screening reports, decision notes tied to written criteria, and adverse action notice if applicable.

- Use a retention schedule consistent with your jurisdiction and risk posture.

If it is not documented, it did not happen in a dispute.

9. Rushing the Process

Approving the first applicant who meets minimum thresholds because of vacancy pressure amplifies every other screening mistake: missed fraud, missed eviction history, inconsistent exceptions, and incomplete verification.

Vacancy is expensive, but a fast wrong approval is more expensive. Eviction and turnover costs can easily exceed several months of rent on a single unit. A landlord who skips reference calls because the applicant "seems straightforward" may miss repeated lease violations the prior landlord would have disclosed. Accepting an incomplete application to "hold the unit" creates inconsistency and potential Fair Housing risk.

How to fix it:

- Create a standard timeline: same-day application receipt, 24–48 hours for verification, decision only when the file is complete.

- Use a "missing items" checklist and do not begin screening until authorization and core documents are received.

Speed is an advantage only when the process is complete.

10. Not Understanding What to Look for in a Screening Report

Receiving a screening report without knowing which sections matter, what is legally actionable, or how to resolve discrepancies leads to wrong approvals and wrong denials. Tenant screening reports can contain accuracy issues and dispute friction that landlords need to understand before acting.

Credit may show stable payment history while address history does not match claimed residency. An eviction section may appear clear while public records show a filing under a prior address or name spelling. A criminal record may fall outside the legally usable time window in your jurisdiction.

How to read a screening report:

- Identity and address trace: Confirm the applicant's stated history aligns with report data.

- Eviction history: Check filings and judgments and reconcile name variations.

- Credit tradelines and collections: Focus on landlord-related collections and recent delinquencies rather than score alone.

- Criminal history: Apply local law and individualized assessment where required.

- Consistency check: Does income, employment, and address history match the application?

A screening report is a set of signals. Your job is to reconcile them into a defensible decision.

Checklist: Standardized Tenant Screening Process

Pre-Application

- Written tenant selection criteria published (income, credit approach, rental history, evictions, criminal history approach, occupancy, assistance animal handling per law)

- Criteria applied consistently to every applicant

- Local rules confirmed: source-of-income protections, fair chance/criminal history limits, application fee rules

Application Intake

- Complete application required for every adult occupant

- FCRA-compliant disclosure and written authorization collected before ordering any consumer report

- Identity basics verified (matching name, date of birth, address history)

Verification

- Income verified by income type (W-2, 1099, self-employed, fixed income)

- Paystub math, deposit patterns, and employment details cross-checked

- Employer contact information independently verified

- Fraud indicators flagged: urgency pressure, inconsistent formatting, refusal to provide originals

Screening Reports

- Eviction history reviewed: filings and judgments, name variations, recentness

- Credit analyzed beyond score: recent delinquencies, landlord collections, debt load

- Criminal history reviewed per local rules with individualized assessment where required

Decision and Documentation

- Decision documented and tied to written criteria (approve, conditional, deny)

- Reports, notes, and verification artifacts saved in screening file

- FCRA adverse action notice sent if denying or setting materially worse terms based on a report

- Outcomes tracked (late pay, notices, eviction) to refine criteria over time

Common Questions About Tenant Screening

What are the most common tenant screening mistakes landlords make?

The most frequent errors are screening without written criteria, skipping eviction history checks, over-relying on credit scores, inadequate income verification, and FCRA non-compliance. Each creates direct financial exposure through higher default rates, eviction costs, and legal liability. A documented, consistent process addresses all five.

How should a landlord screen applicants with no credit history?

Evaluate verifiable stability instead of forcing a score-only decision. Focus on income verification depth, rental payment history where available, and landlord references. Rental payment data is a strong predictor of tenant performance. Document the alternative criteria and apply it consistently to avoid Fair Housing risk.

Can a landlord deny an applicant based on criminal history?

Blanket criminal record bans create disparate impact risk under the Fair Housing Act. Many jurisdictions require individualized assessment before adverse action based on criminal history. Where allowed, evaluate recency, severity, and relevance to legitimate safety concerns, and document the reasoning.

What must be included in an adverse action notice?

When denying or imposing materially worse terms based on a consumer report, the FCRA requires an adverse action notice. It should include the reason for denial, the name and contact information of the consumer reporting agency, and a statement of the applicant's right to dispute. Store a copy in the applicant's file.

How can landlords detect fraudulent rental applications?

Cross-check pay stubs against YTD totals, verify employment through independently sourced contact information, and compare bank deposit patterns to stated income. Inconsistent document formatting, urgency to skip verification, and refusal to provide originals are common red flags.

Is a credit score enough to evaluate a rental applicant?

A credit score alone does not predict rental performance. It measures credit risk, not rent payment behavior. An applicant with a high score but recent late payments and high utilization may be riskier than an applicant with a lower score and stable rental history. Evaluate tradeline quality, landlord-related collections, and debt-to-income alongside the score.

Are there limits on how much a landlord can charge for an application fee?

Yes, in some jurisdictions. Several states and cities cap or regulate application fees. Disclose the fee upfront and ensure it is applied consistently and lawfully. Check your state and local statutes to confirm the current limit, if any.

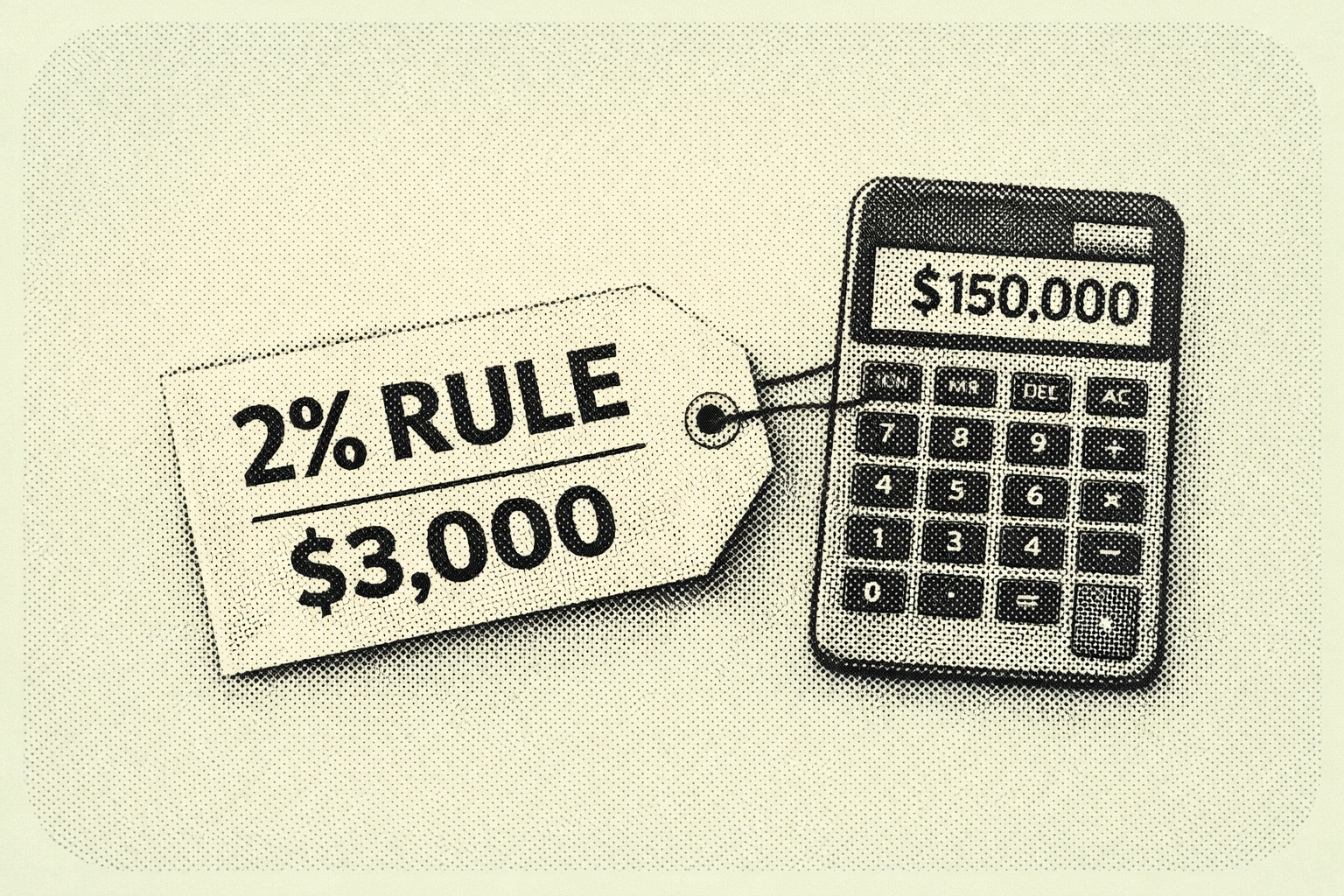

What Is the 2% Rule in Rental Property?

When you self-manage a portfolio, even just a few units, the hardest part of buying a rental property is not finding listings. It is filtering dozens of maybe deals down to the few worth your time. Between listing photos, rough rent estimates, shifting interest rates, and market headlines, you can burn hours underwriting properties that were never going to cash flow.

That is why rent-to-price rules of thumb exist. They are not meant to replace real analysis. They help you triage: move quickly, rule out obvious mismatches, and focus your energy where you will get the best return. Among these quick filters, the 2% rule is the most aggressive.

The formula is simple. A property's monthly gross rent should be at least 2% of your total acquisition cost, meaning purchase price plus rehab. If you buy for $150,000 all-in, you would want $3,000 per month in rent.

The catch is that after post-2020 home price increases, the classic 2% benchmark is now rare in many U.S. metros, especially coastal and high-growth markets. That does not make it useless. It means you need to understand when it works, where it breaks, and what to do next once a property passes or fails the screen.

What the 2% Rule Is and What It Is Not

The 2% rule is a rent-to-cost test: a quick rental income metric that compares gross monthly rent to what you invested to acquire the property. Most definitions specify total acquisition cost as purchase price plus rehab needed to get the unit rent-ready. In real-world underwriting, you will often also want to consider closing costs, initial leasing costs like paint and lock changes, and immediate safety or code items.

The higher the monthly rent is relative to what you paid, the more room you typically have to cover operating expenses including taxes, insurance, repairs, vacancies, and property management, and still produce cash flow. That is why percentage rules became popular among cash-flow investors in lower-cost Midwestern markets and why they have been widely discussed in landlord education communities since the early 2000s.

Here is what the 2% rule does not do. It does not account for local expense structures, which can vary dramatically by county and state. It does not incorporate financing terms including interest rate, down payment, or loan structure. It does not measure profitability directly because it ignores vacancy, maintenance, capital expenditures, and tenant turnover. And it does not capture appreciation expectations, which research has shown can be a major component of long-run returns.

Because of those omissions, the 2% rule is a fast smell test, not a full inspection. Use it as a starting filter, then validate the deal with expense-based metrics like cap rate, cash flow projections, and debt service coverage analysis.

How to Use the 2% Rule Without Fooling Yourself

Step 1. Start With the Exact Formula and Define Your All-In Cost Up Front

The calculation is straightforward.

Rent-to-cost ratio = Monthly gross rent divided by total acquisition cost.

A property meets the 2% rule if monthly gross rent is at least 2% of total acquisition cost.

Run the metric two ways for consistency. The core test uses purchase price plus rehab, which aligns with the most common definition. The conservative test adds estimated closing costs and initial leasing expenses, which is closer to your true cash invested. Rules of thumb are already blunt instruments. If your inputs vary deal to deal, the rule produces noise instead of signal.

Step 2. Use Current Market Anchors to Set Realistic Expectations

The biggest reason landlords get discouraged by the 2% rule is that they apply it in markets where it is structurally unlikely. Recent Zillow data illustrates why this matters.

Los Angeles shows average home values near $941,985 and average rents around $2,658, producing a rent-to-value ratio of roughly 0.28% per month. Seattle shows average home values near $848,869 and average rents around $2,258, producing roughly 0.27% per month. Indianapolis shows average home values near $223,231 and average rents around $1,463, producing roughly 0.66% per month. Cleveland shows average home values near $113,669 and average rents around $1,250, producing roughly 1.10% per month. Tampa shows average home values near $369,079 and average rents around $2,213, producing roughly 0.60% per month.

These are broad metro averages, not deal-specific comps. But they illustrate a critical point: the same 2% threshold implies dramatically different feasibility depending on local prices, rent ceilings, and supply and demand conditions.

Instead of asking whether a market meets 2%, ask what rent-to-cost ratios are typical there, and if 2% is unrealistic, what threshold reliably indicates a workable cash-flow candidate. Many modern investor discussions treat 1% or even 0.8% as more realistic in many areas, while still using 2% as a home-run screen in low-cost or distressed value-add contexts.

Step 3. Run the Calculation Step-by-Step: A Midwest Value-Add Example

A landlord finds an older house in the Cleveland area priced below the broader metro average, needing moderate rehab.

Purchase price: $95,000. Rehab to rent-ready: $15,000. Total acquisition cost: $110,000. Expected monthly gross rent: $1,950.

Dividing $1,950 by $110,000 produces a ratio of 1.77% per month. To meet the strict 2% rule, the property would need $2,200 per month in rent.

This property fails the 2% threshold, but it is close. In many real-world scenarios, a 1.7% to 1.8% ratio may still be worth full underwriting, especially if the rehab estimate is tight, tenant demand is strong, and the neighborhood risk profile fits your management capacity. Cleveland's broader metro average produces about 1.10% rent-to-value. A deal at 1.77% is significantly above that average, suggesting a favorable purchase basis, above-average achievable rent, or both. That is often what a good deal looks like in a low-cost market: you are outperforming the typical rent-to-price relationship, not chasing a mythical 2% in every zip code.

Step 4. Contrast With a High-Cost Coastal Market

A landlord evaluates a small duplex in Los Angeles with strong tenant demand but a high acquisition cost.

Purchase price: $950,000. Rehab and turnover work: $25,000. Total acquisition cost: $975,000. Expected monthly gross rent for both units combined: $5,400.

Dividing $5,400 by $975,000 produces a ratio of 0.55% per month. To meet the 2% rule, the property would need $19,500 per month in gross rent, which is far beyond typical long-term rents for most small multifamily properties in any market.

In coastal markets, investors often justify acquisitions through a different return mix: lower current yield paired with potential long-term appreciation, rent growth, tax advantages, and inflation hedging. Academic work on rent-price dynamics confirms that expected capital gains can heavily influence buying behavior even when rent ratios are low. That is precisely why simplistic ratios can mislead if treated as universal laws rather than market-relative tools.

Step 5. Compare the 2% Rule to the 1% Rule

The 1% rule is the more commonly cited version: monthly gross rent should be at least 1% of total acquisition cost. It became widely popular through mainstream landlord education and investor communities and is generally treated as a first-pass filter before deeper underwriting.

The practical difference comes down to thresholds. The 2% rule is a very high bar, often indicating a low purchase price relative to rent, significant distress or value-add, or a higher-risk area where prices are low for a reason. The 1% rule is still a strong quick screen in many markets but is challenging in most coastal metros given current pricing.

Use both as a funnel. If a deal meets 2%, treat it as a priority but scrutinize neighborhood quality, tenant demand, and deferred maintenance, because too good can mean hidden risk. If it meets 1% but not 2%, underwrite it because it may still cash flow depending on expenses and financing. If it fails 1%, do not automatically discard it in expensive markets, but require a strong alternative thesis: appreciation potential, development optionality, ADU value, or a clear repositioning plan.

Step 6. Cap Rate Versus the 2% Rule: What Each Metric Tells You

Both metrics compress a deal into a single number, but they answer different questions.

The 2% rule uses gross monthly rent and acquisition cost, ignores expenses and financing, and is best as a fast screening tool. Cap rate uses net operating income divided by purchase price, which means it reflects operating reality more accurately because it accounts for taxes, insurance, repairs, management, and other operating costs. Cap rate still ignores financing, but it captures the expense differences that the 2% rule cannot see.

Two properties can have identical gross rent and identical acquisition cost but wildly different cap rates if one sits in a high-tax county, a higher-insurance region, or a property with major capital expenditure coming due. A practical workflow for self-managing landlords: use the 2% or 1% rule to filter, then estimate a quick cap rate to sanity-check the operating story, then run full financing and cash flow projections including cash-on-cash return, debt service coverage, and stress tests.

Step 7. Add Market and Property-Type Nuances

Property taxes and insurance can break a deal that passes the 2% screen. Expense structures vary by location and are not captured in a gross-rent ratio. Never buy the ratio without validating expenses first.

Post-2020 pricing has made 2% rare in many markets. Many landlords now operate with a tiered target: 2.0% as exceptional, typically limited to value-add, distressed, or very low-cost market scenarios; 1.0% to 1.5% as the more common cash-flow hunting range in many non-coastal markets; and 0.5% to 0.9% as common in high-cost metros requiring a different investment thesis.

Property type also matters. A duplex or fourplex may produce more rent per dollar of purchase price than a comparable single-family in the same neighborhood. Some high-demand single-family neighborhoods command a rent premium, but purchase prices often outpace rents, pushing ratios down. Broad Zillow averages in Los Angeles and Seattle confirm this dynamic at the metro level.

2% Rule Quick Screen Template

Use this when scanning listings or reviewing off-market leads. Apply the same inputs and the same math consistently so you do not treat deals differently based on how much you like them.

Inputs: Purchase price. Rehab to rent-ready. Closing and initial leasing costs (optional but recommended). Projected monthly gross rent.

Calculations: Core all-in cost equals purchase price plus rehab. Core rent-to-cost ratio equals monthly rent divided by core all-in cost. Conservative all-in cost adds closing and initial costs. Conservative rent-to-cost ratio equals monthly rent divided by conservative all-in cost.

Decision rules: At 2.0% or above, flag as priority and proceed to full underwriting, but scrutinize neighborhood quality, deferred maintenance, and confirmed rent comps. Between 1.0% and 1.99%, underwrite the deal because it may be viable depending on expenses and financing. Below 1.0%, proceed only with a clear alternative thesis covering appreciation, redevelopment potential, exceptional rent growth, or a positioning plan that supports the acquisition at that price.

Next numbers to pull before making an offer: Rent comps for the same bedroom and bathroom count in similar condition. Taxes and insurance estimates using local sources rather than national averages. A rough annual expense budget covering maintenance, reserves, and vacancy. A quick cap rate calculation to compare against what the rent-to-cost ratio suggests.

Frequently Asked Questions

Is the 2% rule still realistic in 2026?

In many U.S. markets, especially high-cost coastal metros, the traditional 2% rule is rarely achievable for standard long-term rentals because prices have outpaced rent growth. Zillow's broad metro data illustrates the gap clearly: in Los Angeles, average home values near $941,985 paired with average rents around $2,658 produce a rent-to-value ratio far below 1%, let alone 2%. That said, 2% can still appear in specific situations including distressed purchases, heavy value-add rehabs, low-cost neighborhoods, and certain rental operations. Use it as a home-run screen rather than a universal expectation.

Does meeting the 2% rule guarantee positive cash flow?

No. The 2% rule is based on gross rent and acquisition cost and ignores operating expenses and financing entirely. A property can pass the screen and still cash flow poorly if taxes, insurance, maintenance, utilities, or turnover costs are high, or if financing terms are unfavorable. Treat it as the first filter, then validate the deal with expense-based metrics like cap rate and a full financing-based cash flow model.

What is the difference between the 1% rule and the 2% rule?

They are the same concept with different thresholds. The 1% rule says monthly gross rent should be at least 1% of total acquisition cost. The 2% rule uses 2% and is therefore much stricter. In today's pricing environment, many investors view 1% as challenging but sometimes workable in lower-cost markets, while 2% is often limited to unusually strong cash-flow deals or higher-risk areas.

If my market cannot hit 1% or 2%, what should I use instead?

Do not force a national rule onto a local market. In expensive metros, broad market data shows rent-to-value ratios closer to a fraction of 1% at the metro level. In those environments, shift your screening toward realistic cap rate estimates, conservative cash flow after financing, and a clearly articulated long-term thesis covering appreciation, rent growth, and repositioning potential. Percentage rent rules do not capture expected capital gains, which research confirms can be a major driver of investor returns in high-cost markets.

If you want to track rent-to-cost ratios alongside the operating metrics that actually drive long-term performance, book a demo to see how Shuk helps landlords monitor income trends, vacancy, and portfolio health from one place.

How to Reduce Vacancy Time for Rental Properties

Vacancy time is the period a rental unit remains unoccupied between tenants. It directly impacts landlord cash flow by creating gaps in rental income while fixed costs continue. For property managers handling multiple units, reducing vacancy time from 40 days to 20 days can protect thousands in annual revenue.

What Causes Extended Vacancy Periods

National data shows rental listings typically remain active for 30-40 days before filling. Extended vacancies beyond this benchmark often result from delayed tenant outreach, reactive marketing strategies, or inefficient turnover workflows.

Turnover costs average $3,872-$4,000 per vacancy when accounting for lost rent, repairs, marketing, and administrative time. For independent landlords managing 2-5 units, one extended vacancy can eliminate quarterly profits.

Start Renewal Conversations 90-120 Days Early

Industry research consistently shows that renewal outreach beginning 90-120 days before lease expiration significantly increases retention rates. Early communication prevents last-minute surprises and gives landlords time to address tenant concerns.

Track renewal signals through tenant payment patterns, maintenance request frequency, and engagement levels. Create a simple pipeline categorizing tenants as Interested, Unsure, or Likely Leaving based on responses to structured check-ins.

Use renewal workflows with automated reminders at 90, 60, and 30 days before expiration. Offer clear renewal options with specific terms rather than waiting for tenants to initiate conversation.

Implement Year-Round Marketing Systems

Maintaining active listings year-round builds prospect pipelines before units become vacant. This approach prevents starting marketing from zero when turnover occurs, particularly critical during slower seasonal periods.

Create "coming soon" listings 45-60 days before known move-outs. Include virtual tour links, detailed unit specifications, and clear application requirements to pre-qualify prospects.

Track inquiry-to-showing and showing-to-application conversion rates monthly. If inquiries remain high but applications stay low, screening criteria may lack clarity or unit presentation may not match marketing promises.

Reduce Application and Screening Friction

Application delays extend vacancy time unnecessarily. Digital applications with automated screening reduce processing time from 5-7 days to 24-48 hours while improving applicant experience.

Enable self-showing options through lockbox systems or smart locks for qualified prospects. This removes scheduling constraints that slow the leasing process, particularly for working renters.

Offer electronic lease signing to eliminate coordination delays. Combined with digital payment collection, this approach can reduce lease execution time from days to hours.

Standardize Turnover Workflows

Make-ready delays directly extend vacancy time. Schedule pre-move-out inspections 30 days before tenant departure to identify needed repairs and pre-book vendors.

Create a turnover checklist covering lock changes, safety inspections, repairs, cleaning, and final photography. Target same-day listing publication after make-ready completion.

Track make-ready duration as a performance metric. Properties consistently completing turnover within 7-10 days reduce aggregate vacancy time significantly across portfolios.

Use Tenant Polling to Forecast Moves

Structured tenant check-ins at 120 and 60 days before lease expiration reveal intent before formal notice periods. This early visibility allows landlords to begin marketing and screening while units remain occupied.

Ask specific questions about renewal likelihood, satisfaction drivers, and potential improvement areas. Responses categorize tenants for targeted follow-up and help identify retention opportunities.

Communication quality and maintenance responsiveness consistently rank as top retention factors in industry research. Use polling data to prioritize operational improvements that reduce turnover.

Track Days-on-Market as Primary KPI

Days-on-market measures time from listing publication to lease signing. Monitoring this metric monthly identifies patterns in seasonal demand, pricing effectiveness, and marketing quality.

Benchmark against the 30-40 day national average while accounting for local market conditions. Units consistently exceeding benchmarks indicate issues with pricing, presentation, or application processes.

Supplement days-on-market tracking with renewal rates and turnover costs per unit. These three metrics together reveal the true financial impact of vacancy management strategies.

Frequently Asked Questions

How long should rental vacancies typically last?

Rental vacancies typically last 30-40 days nationally. This benchmark reflects time from listing to lease signing under normal market conditions. Units exceeding 40 days should be evaluated for pricing accuracy, listing quality, or showing availability issues that may be extending vacancy time unnecessarily.

What is the best way to reduce tenant turnover costs?

Start renewal outreach 90-120 days before lease expiration and address tenant concerns proactively. Early communication increases retention odds while reducing emergency turnover scenarios. Pair renewal timing with service quality improvements like faster maintenance response and clear communication channels to strengthen tenant satisfaction.

Should landlords market vacant units year-round?